Public Finances: How can we make them sustainable and invest in Guernsey's future?

Changes in Guernsey’s population are driving demand for some public services, especially health care and pensions. As costs rise, we also need to address an under-investment in Guernsey’s infrastructure, including housing, education and health facilities.

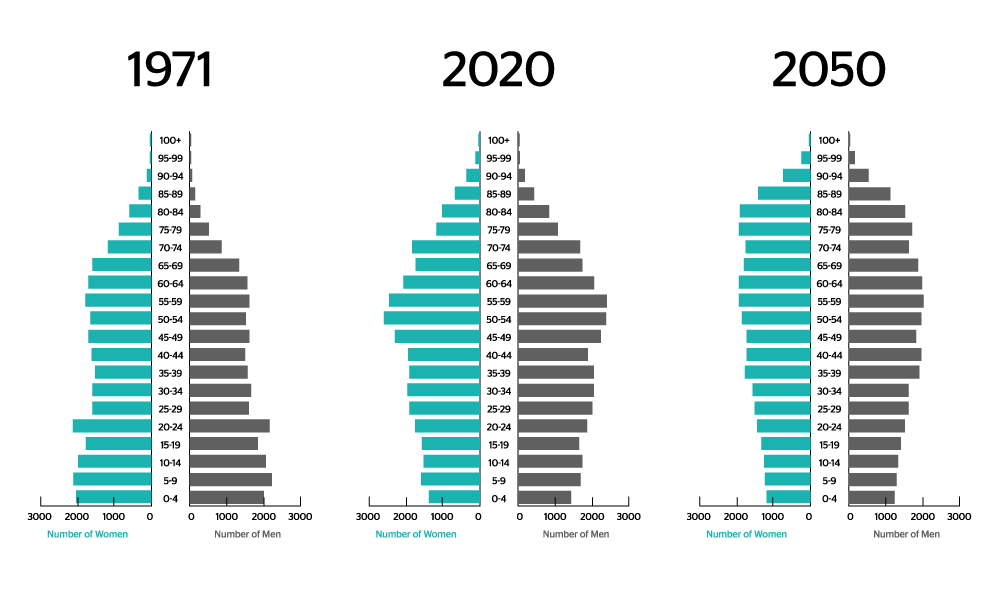

The change in the make-up of Guernsey’s population is one of the biggest challenges we face over the coming years. As a result, a funding shortfall is forecast to rise to about £100m a year by 2040.

Changes to the make-up in our population

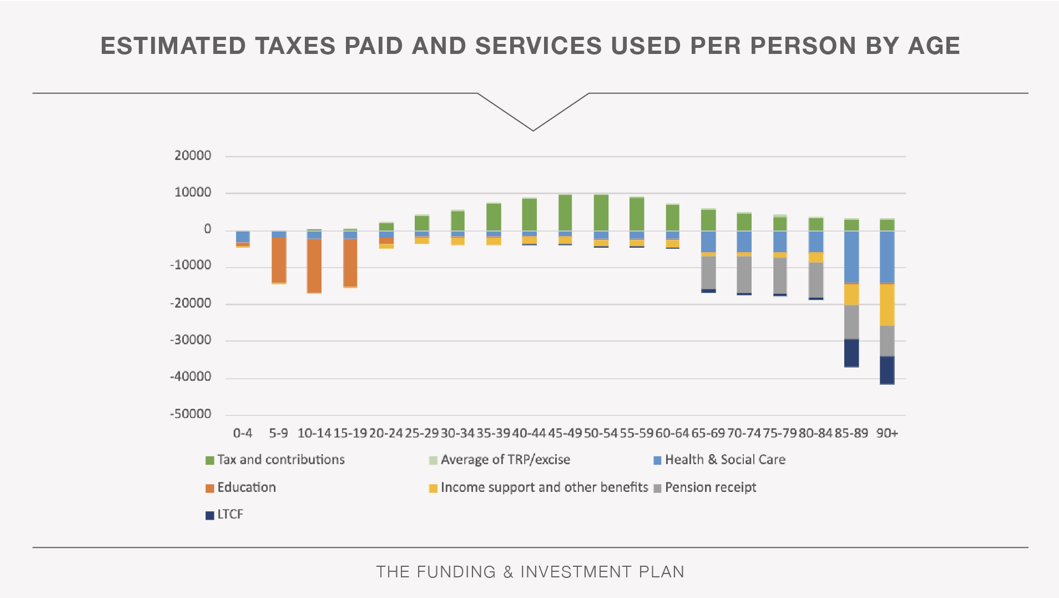

All Islanders make a valuable contribution to funding our public services and have done so throughout their lives. But inevitably as we each get older we use more services. This chart shows how much on average people in each age group contribute compared to the cost of the main services they use. As the number of people in the 20 to 64 age groups decreases and the number in the 65+ increases, it reduces income and increases costs.

Investing in our infrastructure

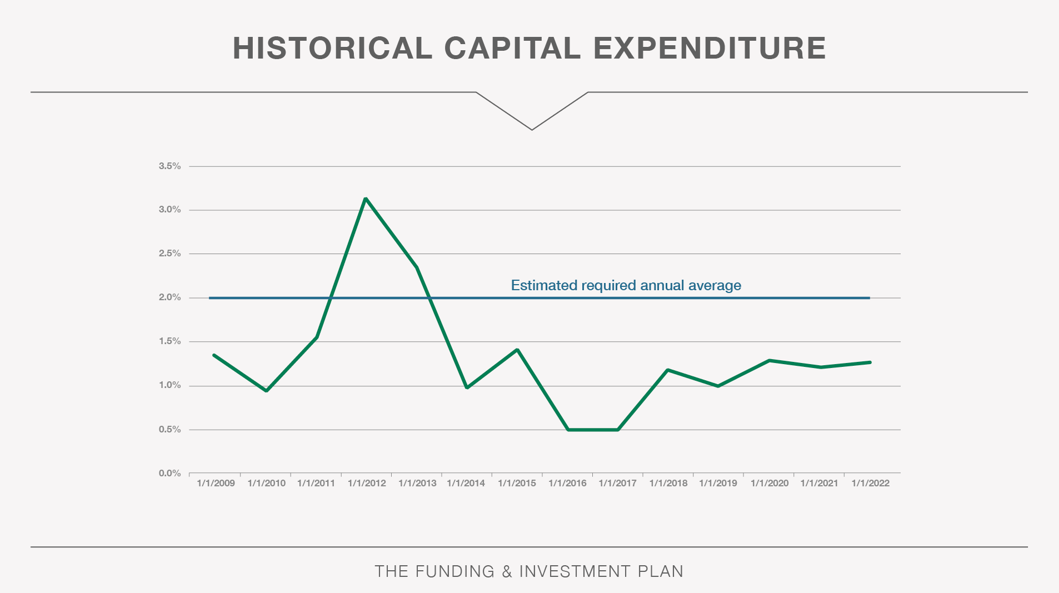

The States aims to invest an average of 2% of GDP in the Island’s infrastructure each year, so that our public facilities including education and health facilities, ports, sea defences and other essentials are fit-for-purpose. However for years, the States have not invested enough to meet this 2% of GDP target.

The need to spend on infrastructure, which increases following years of under-investment, adds to the pressures on public finances.

What is the States doing about it?

The Funding & Investment Plan

In October 2023, the States held its most recent debate on the Funding & Investment Plan and the Capital Portfolio, two documents which together set out which major infrastructure projects the States will undertake and how it will fund them.

As part of the debate, States Members discussed a number of possible reforms to the tax system which would have raised more revenue and moved Guernsey towards a more sustainable financial position. However the States did not agree any of these. Instead it agreed that the Policy & Resources Committee should return by September 2026 with new proposals for how to address the deficit and put public finances into a sustainable position.

The States also agreed that some limited revenue raising measures should proceed:

- an additional £15m per annum from corporate taxes, largely from the OECD’s ‘Pillar 2’ initiative

- £10m a year in new income from transport related taxes, initially an annual charge on vehicle ownership

- £10m of annual savings in the cost of public services, delivered over the next 5 years

The States also agreed:

- Annual investment in the development of policy of £3m a year to ensure that government priorities for improvement can be progressed

- Continued investment in routine capital replacements of £20m per year, over the rest of this term

- Use of £160m of the proceeds of the existing bond towards the delivery of capital priorities

- Preserving the limited States reserves this term to give some financial resilience and ensure the next States have funding available for their priorities

The States also agreed how it intended to prioritise its list of major infrastructure projects:

The States agreed the deliver of the following 17 ‘in-flight’ projects at a cost of £96m. These projects are already underway with work having begun or contracts already agreed:

- Our Hospital Modernisation Phase 1

- Electronic Patient Record

- Digital Infrastructure

- Funding Affordable Housing Developments Programme

- IT Transformation

- Revenue Service Programme

- Virtual Machine

Environment (VME) Replacement - Guernsey Registry IT Systems Replacement

- Online Passport & Workflow System

- Footes Lane Refurbishment

- Sarnia Cherie Ballast Water Management System (BWMS)

- Mont Crevelt Breakwater Reinstatement

- Transforming Education Digital (secondary and primary)

- SMART Court Phase 1

- MyGOV Programme

- Havelet Slipway Repairs

- Tetra Public Safety Network (PSN)

The States agreed to proceed with the following list of projects as planned as a priority. The combined cost is around £208m, plus £30m contingency for inflation

- Property Rationalisation Phase 2

- Clinical & Animal Waste Solution

- Community Services Children & Families Hub

- Central Stores - Supply Chain Relocation

- Bridge Regeneration (Housing and SS Bridge Flood Defences)

- Future Harbour Requirements – Survey work

- Alderney Airport Pavements Rehabilitation

- Repair/Replacement of Castle Emplacement Bridge

- Our Hospital Modernisation Programme – Phase 2 and associated works

The States agreed these projects should go ahead but believed the scope of the works involved could be reduced or done in a way that is more cost-effective, and it has agreed £5m for these projects.

- Guernsey Airport Pavements Rehabilitation (PFOS)

- Fermain Wall Repair (reduced scope to realignment of cliff path only)

Transformation spend is for one-off initiatives that aim to reshape public services. These initiatives currently fall into Education, Sport & Culture, Health & Social Care and Corporate Services.

- Transforming Health & Social Care

- Transforming Education

- MyGov – Transforming Government Services – Next Phase

The following schemes which were previously in the States agreed capital portfolio no longer have any funding provided in this term.

- SAP Roadmap

- Inert Waste Facility

- Transforming Education Programme (Post-16 Campus at Les Ozouets’ and other secondary school changes)

- Bus Fleet Replacement Phase 3

- Smart Court Phases 2 & 3

These de-funded schemes have been added to the pipeline list for prioritisation in future terms. A total of £1m is available for scoping and planning work for the pipeline schemes:

- CCTV Replacement

- Coastal Flood Defences

- Guernsey Airport Runway Infrastructure

- Home Affairs Estate Rationalisation

- Community Hub (Health and Social Care)

- HSC Digital Roadmap

- Future Guernsey Dairy

- Future Harbour Requirements

- Our Hospital Modernisation – Pathology

- SAP Roadmap

- Future Inert Waste Facility

- Transforming Education Programme (Post-16 Campus at Les Ozouets’ and other secondary school changes)

- Bus Fleet Replacement Phase 3

- SMART Court Phases 2 & 3

Independent Fiscal Policy Panel report

Shortly before the debate on the Funding & Investment Plan, an independent panel of economists, the Fiscal Policy Panel, carried out a report providing an impartial analysis of the fiscal challenges facing Guernsey. The panel provided their opinion on whether the options presented as solutions to the fiscal challenges were appropriate, viable and sustainable.

How will cost reductions be achieved?

The work to identify cost reductions of £10m - £16m per year is being led by a sub-committee of the Policy & Resources Committee. Its members are:

- Deputy Dave Mahoney (Chair)

- Deputy Sasha Kazantseva-Miller

- Deputy Carl Meerveld

- Deputy Simon Vermeulen

- Mr Dave Beausire

As well as engaging with States Committees and individual Deputies, the Sub-Committee has carried out a survey for all Guernsey and Alderney residents inviting their suggestions for how the cost of public services should be reduced. 637 people responded to the survey, providing 1,416 suggestions.

A sister survey was also carried out for public sector employees to make suggestions. 196 people responded to this survey, making a total of 394 suggestions.

The Sub-Committee has published some initial insights on the broad themes that are beginning to emerge as its analysis of the suggestions gets under way.

The Sub-Committee is continuing to assess the responses, and will make recommendations to the States for where the reductions should happen in the early part of 2024.

Review of other tax options

A separate sub-committee of the Policy & Resources Committee is looking at other ways of raising revenue, including progressing the work underway to raise more money from the corporate sector, while maintaining Guernsey’s competitive position and compliance with international standards. As part of this, the sub-committee was directed by the States to engage with industry, Jersey and the Isle of Man to develop proposals.

The sub-committee is led by Deputy Mark Helyar, Vice-President of the Policy & Resources Committee. Also appointed to the sub-committee are:

- Deputy Lyndon Trott

- Deputy Nick Moakes

- Mr Andrew Niles

The work of this sub-committee to date has involved:

- Exploring options for changes within the current domestic TRP system

- Reviewing other options around property taxes

- Exploring scope for raising additional revenues from the corporate sector through registry fees and/or a business levy

- Examining the extent of ‘rolled up profits’ and whether any steps need to be taken to encourage distribution

- Looking at the possibilities for extending the scope of the current 10% and 20% rates of income tax for corporate entities

- Launching a consultation on a possible transaction tax similar to the ‘Tax D’abonnement’ in Luxembourg

2024 Budget

The 2024 Budget was debated and approved by the States of Deliberation in November.

While the Funding & Investment Plan asked the States to make longer-term decisions about the sustainability of public finances, reforming the tax system and how to fund investment in public infrastructure, the 2024 Budget also takes into account the current unsustainability and includes measures for 2024 that are geared towards raising more revenue from those who can most afford it.

The full Budget and voting records for all of the decisions made by the States of Deliberation is available here: States Meeting on Tuesday 7th November 2023 (Annual Budget for 2024) - States of Guernsey (gov.gg)